Print

PrintGarrett Muzikowski is a Senior Director and Hetal Kanji is a Director at FTI Consulting. This post is based on their FTI Consulting memorandum. Related research from the Program on Corporate Governance includes Social Responsibility Resolutions (discussed on the Forum here) by Scott Hirst.

2023 has seen investors support significantly less environmental and social proposals in past years. While overall support has dropped, issuers should understand important macro, regional, and issue specific factors driving this trend as they prepare for their off-season engagement efforts and 2024 proxy season.

The volume of shareholder proposals looking to address ESG issues varies between the US and Europe – driven in part by proposals in the US being non-binding, as opposed to legally binding in parts of Europe, and the requirements for placing a proposal on the ballot in each region. While the differences in the number of shareholder proposals is explained by the different regulatory environments, the factors influencing shareholder support may not be as clear.

In the US, the decrease in average investor support of environmental and social shareholder proposals during 2022 was largely attributed to a change in SEC rules allowing more prescriptive proposals to reach the ballot. The impact of the war in Ukraine on the global economy also led investors to give companies more leniency on their climate initiatives. Additional factors relate to companies demonstrating progress in addressing the issue at hand, or reaching a compromise with the proponent in exchange for withdrawing a proposal.

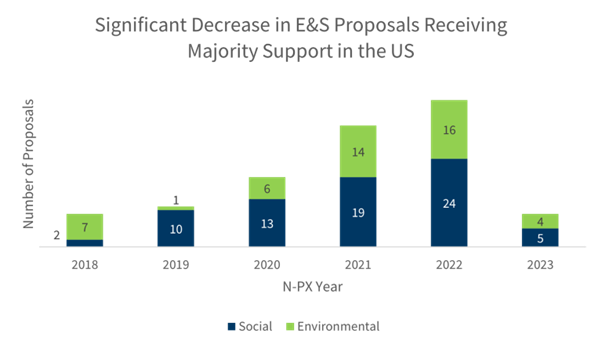

2023 saw another drop in investor support, which was driven by a combination of issues, but principally by the anti-ESG agenda. On one hand, the number of proposals filed by anti-ESG proponents has grown significantly in recent years, however, their proposals often see low support. Since 2018, anti-ESG proposals received, on average, 6.7% support from shareholders. This dropped to 5.1% support during this year’s proxy season. Based on this data, we may assert that the impact on the corporate governance landscape from the anti-ESG momentum is not measured by the number of anti-ESG proposals filed, but by the number of ESG proposals that were not supported by institutional investors. The scrutiny on institutional investor vote behavior across a range of E, S and G matters, by the anti-ESG activists, has caused institutional investors to support less environmental and social proposals in 2023. In the U.S., only ten environmental or social proposals received majority support this N-PX year*.

While this decrease is certainly attributed to other factors like continued progress in company disclosure and more prescriptive proposals reaching the ballot, it’s clear anti-ESG pressure has reached large institutional investors.

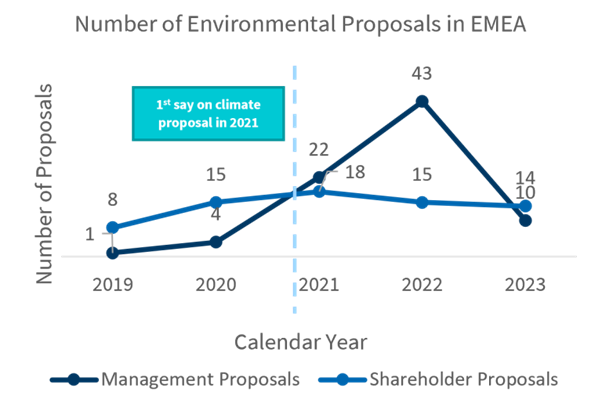

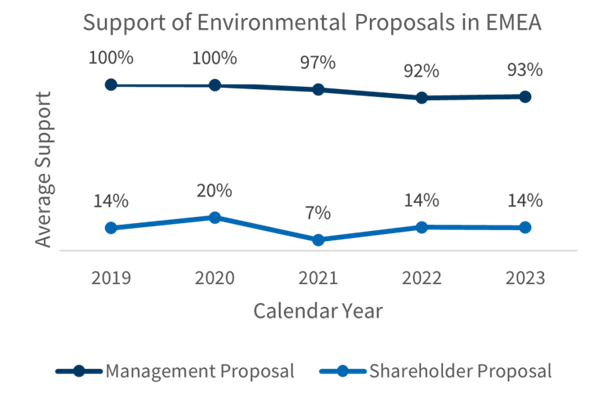

Given the significant shareholding of large US institutional investors across European equities, the anti-ESG backlash in the US has likely impacted outcomes at European AGMs. Shareholder proposals in Europe have been generally related to requests for companies to amend or adopt a change policy, publish a climate change report or more widely to develop an environmental policy. The number and support for these proposals has steadily decreased since 2021, the year where a significant number of companies first submitted their own management sponsored climate resolutions, deemed “Say on Climate”. This increase in the number of management sponsored proposals was reflective of companies’ inclination to put forward their own climate resolutions rather than have them put forth by an activist shareholder.

The number of management-sponsored environmental proposals, which comprise of either say-on-climate proposals or proposals seeking shareholder approval of companies’ sustainability report, increased sharply in 2021 and 2022 before falling off in 2023. As say-on-climate proposals become more common, institutional investors have refined their approach and increased scrutiny, evidenced by a general decrease in support levels. 2023’s slight uptick in support was likely driven by the fact that none of the oil and gas majors submitted similar proposals this year.

Source: Insightia data

Let’s look deeper into what proposals saw more support in 2023:

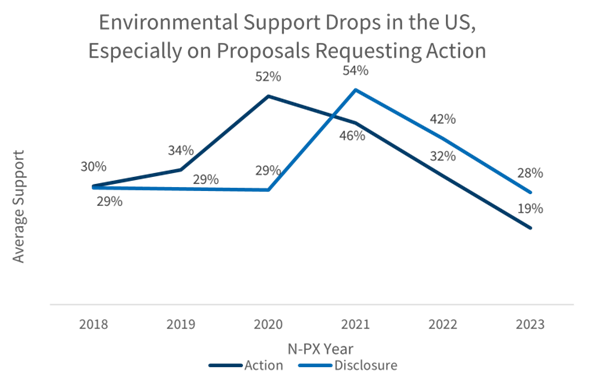

US Environmental Proposals: Decrease Across the Board, Especially on Action

All four environmental proposals that passed this year requested additional disclosure from the target company, noteworthy compared to other proposals that request companies take a specific action. This bifurcation caught our eye and is something we analyzed more closely. It’s true – investors are more likely to support environmental disclosure requests than to push companies to take a specific action, in line with a general preference from investors to review increased information as opposed to directly manage investee companies:

EMEA Environmental Proposals: Binding Nature of Scope 3?

This year, the Dutch activist shareholder, Follow This (the ‘proponent’), targeted five of the oil ‘super-majors’ – Shell, BP, Exxon, Chevron, TotalEnergies (‘Total’) as the largest and most influential companies with an impact on global emissions. The proponent submitted a shareholder proposal to each of these companies’ ballots, calling for the companies to set and disclose a ‘medium-term Scope 3 emissions reductions target’ that is in line with the Paris Agreement. The table below sets out the outcomes at each of these AGMs:

Source: Insightia data

It is worth noting from the above that the proposal filed at Total’s AGM was the only European proposal that was non-binding. Unsurprisingly, it was also the only proposal this year that received support from ISS and it saw the most support. The 30% support for the shareholder proposal at the Total AGM, highlights the limitations on shareholder interference on strategic matters, which seem to play an important role in proxy advisors’ recommendations and investor action on these matters. More specifically, it also represents both regional differences between the US and Europe, including the recent anti-ESG pressure in the US, and also how investors analyze proposals when they are binding or non-binding.

US Social Proposals: Labor, Labor, and More Labor

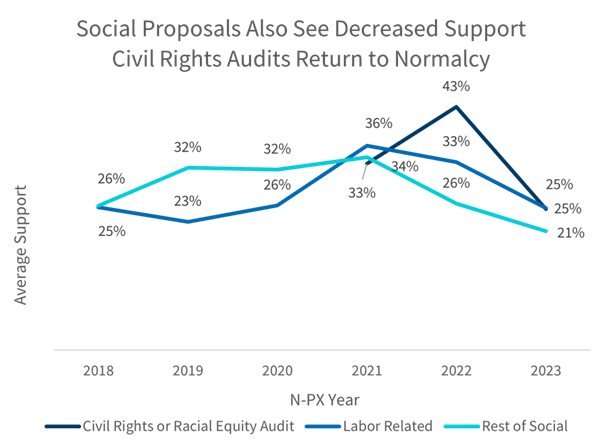

Key social themes that emerge during proxy season tend to lag actual trends in the news and in society by one year. Think about civil rights audits emerging as the main story in 2021 into 2022 after the COVID-19 pandemic and racial injustice coverage in the U.S. the year prior.

Labor-related topics drove news coverage in 2022: inflation affected workers’ living wage, while topics like workers’ safety, benefits, and freedom of association were also hot button issues. It’s no surprise, then, that five of the six majority supported social proposals were on labor related topics. The proposals included a Workplace Health and Safety Audit, a Report on Effectiveness of Diversity Equity and Inclusion Efforts and Metrics, a Report on Prevention of Workplace Harassment and Discrimination, a Report on Gender and Racial Pay Gap, and a Third-Party Assessment on Company’s Commitment to Freedom of Association and Collective Bargaining Rights.

Analyzing overall support trends, civil rights audits’ huge decrease in average support is noteworthy. In N-PX year 2022, a third of all proposals that received majority support were for civil rights or racial equity audits. This year, the highest support any proposal saw on the topic was 40%. While important to note that 18 proposals on the topic were withdrawn, it’s possible anti-ESG pressure on institutional investors led to this decrease in support. Outside of emissions reduction targets, civil rights and racial equity audits were arguably the most scrutinized topic of vocal anti-ESG advocates.

EMEA Social: The Role Cost of Living and Wages Plays in Remuneration

In light of rising inflation, the cost-of-living crisis and a general level of uncertainty in the macroeconomic environment, the Investment Association, a UK trade body representing investors, asked companies to “sensitively” balance the need to continue to incentivize executive performance with the experience of shareholders, employees, and stakeholders most impacted by wider market turbulence. This guidance led a number of investors to publicly note their expectations from remuneration committees on topics like fairness and quantum of executive pay, as detailed in our previous thought leadership piece.

During this year’s AGM season, a coalition of 15 investors and Share Action, an NGO that promotes responsible investment, called on companies to “take decisive action in this AGM season to protect their lowest paid workers during the cost-of-living crisis”. From the proposed changes it is worth noting the focus on paying a real living wage to all employees across the supply chain, where third-party contractors are included, as well as in ensuring fair and accurate contracts, and guaranteed working hours.

Votes – advisory and binding – against payouts to executives and their remuneration policies across the UK and the US, typically draw significant attention. While investors have placed a significant focus on evaluating the fairness and quantum of executive pay, this has come under additional scrutiny, particularly in the context of a difficult macroeconomic environment and cost of living crisis.

Source: Insightia data

In the UK & Ireland, this scrutiny was evidenced by the drop in support for remuneration report proposals. The remuneration report proposal, much like a say-on pay-vote, allows shareholders to opine on executive pay outcomes for the previous year, as well as certain plans for the year after. The remuneration policy vote allows shareholders to vote on the structure of the executive remuneration, which is updated and submitted to shareholder vote at least every three years in the UK.

While investors have placed significant scrutiny on executive pay practices in the past, they are now being called to use their influence to push companies to address pay inequalities, particularly during a cost-of-living crisis. Evidence of this pressure has been clear for a number of years, through the demands from institutional investors that pension for senior executives do not exceed those of the general workforce. The levers to do this are incentivizing long-term fair remuneration policies for companies’ employees and by potentially opposing executive pay packages that are disproportionately higher for executives, akin to ratio concerns in the US. Across the US and EMEA, labor and wages played a role in investor voting behavior in 2023. The nuance, however, is driven by market norms. In the US, investors expressed the importance of labor through shareholder proposals, while in EMEA its importance it could be seen through votes on remuneration. While remuneration might be seen as more of a traditional governance issue, it can also open up companies to criticism from activists, pointing to how Boards are overly deferential to management, at the expense of shareholders.

Looking ahead

Shareholder proposals are an important platform for shareholders to raise issues to a company’s leadership and fellow shareholders, while simultaneously pressurising Boards to act. From 2018 to 2021, proposals generally saw an increase in support and Boards needed to fear the real possibility of a proposal passing. However, as scrutiny on ESG increases, as well as on investor and proxy advisor action generally, along with more prescriptive requests from activists, has led to a significant decrease in shareholder support over the past two years.

Two years of drops in support raises the questions – did rising support for E&S shareholder proposals plateau and is now on a permanent decline? And, as a result, are we likely to see activists change their strategy, either by focusing on different topics, tactics, or by targeting different companies, to drive a rebound in support for shareholder proposals?