Hilary Wiek is a Senior Strategist and Anikka Villegas is an Analyst at PitchBook. This post is based on their Sustainable Investment Survey. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; Does Enlightened Shareholder Value add Value (discussed on the Forum here) by Lucian Bebchuk, Kobi Kastiel, Roberto Tallarita; Reconciling Fiduciary Duty and Social Conscience: The Law and Economics of ESG Investing by a Trustee (discussed on the Forum here) by Max M. Schanzenbach and Robert H. Sitkoff; and Exit vs. Voice (discussed on the Forum here) by Eleonora Broccardo, Oliver Hart and Luigi Zingales.

About the survey

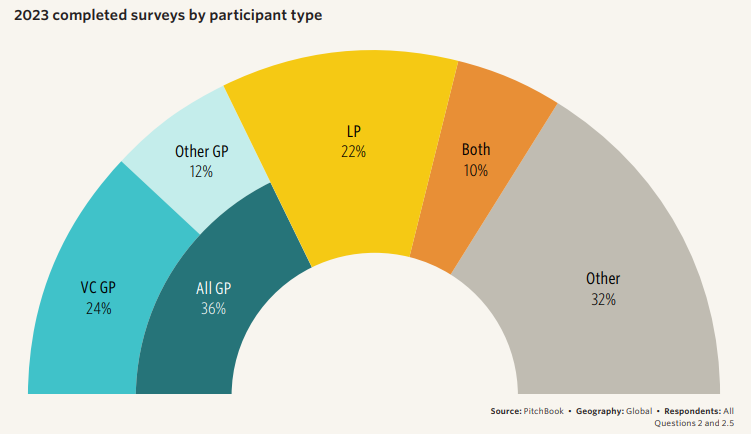

This group of respondents represents the most balanced profile to date for this survey, showing that the interest in sustainable investment issues run far and wide.

Since the release of our last Sustainable Investment Survey report in October 2022, we have been busy with our sustainable investment research efforts. Using our proprietary Impact fund data set utilizing the Global Impact Investing Network’s (GIIN) IRIS+ taxonomy, we updated our reporting on fundraising trends in private Impact fund investing. [1] As a follow-up to 2022’s survey, we took some of the open-ended responses and wrote a report addressing the concerns and criticisms of ESG. In January, we published a piece on sustainable and digital infrastructure in the private markets, noting that infrastructure has not only been expanding as an area of investment, but it is increasingly looking to contribute sustainable solutions to areas like climate change and socioeconomic equality. Finally, we have brought on an emerging technology analyst focused on producing carbon & emissions tech and clean energy work for PitchBook clients.