Matteo Tonello is Managing Director of ESG Research at The Conference Board, Inc., and Jason D. Schloetzer is Associate Professor of Business Administration at the McDonough School of Business at Georgetown University. This post relates to CEO Succession Practices in the Russell 3000 and S&P 500: Live Dashboard, an online dashboard published by The Conference Board, Heidrick & Struggles, and ESGAUGE.

These Key Findings are based on a dataset downloaded on July 6, 2022 from CEO Succession Practices in the Russell 3000 and S&P 500: Live Dashboard. The Live Dashboard is updated weekly with information on succession announcements about chief executive officers (CEOs) made at Russell 3000 and S&P 500 companies; please browse the Live Dashboard for the most current figures. For comparative purposes, the Live Dashboard includes historical data and breakdowns across business sectors (as classified under the Global Industry Classification Standard, or GICS) and company size groups. See Using this Dashboard for more details.

The project is conducted by The Conference Board and ESG data analytics firm ESGAUGE, in collaboration with executive search firm Heidrick & Struggles.

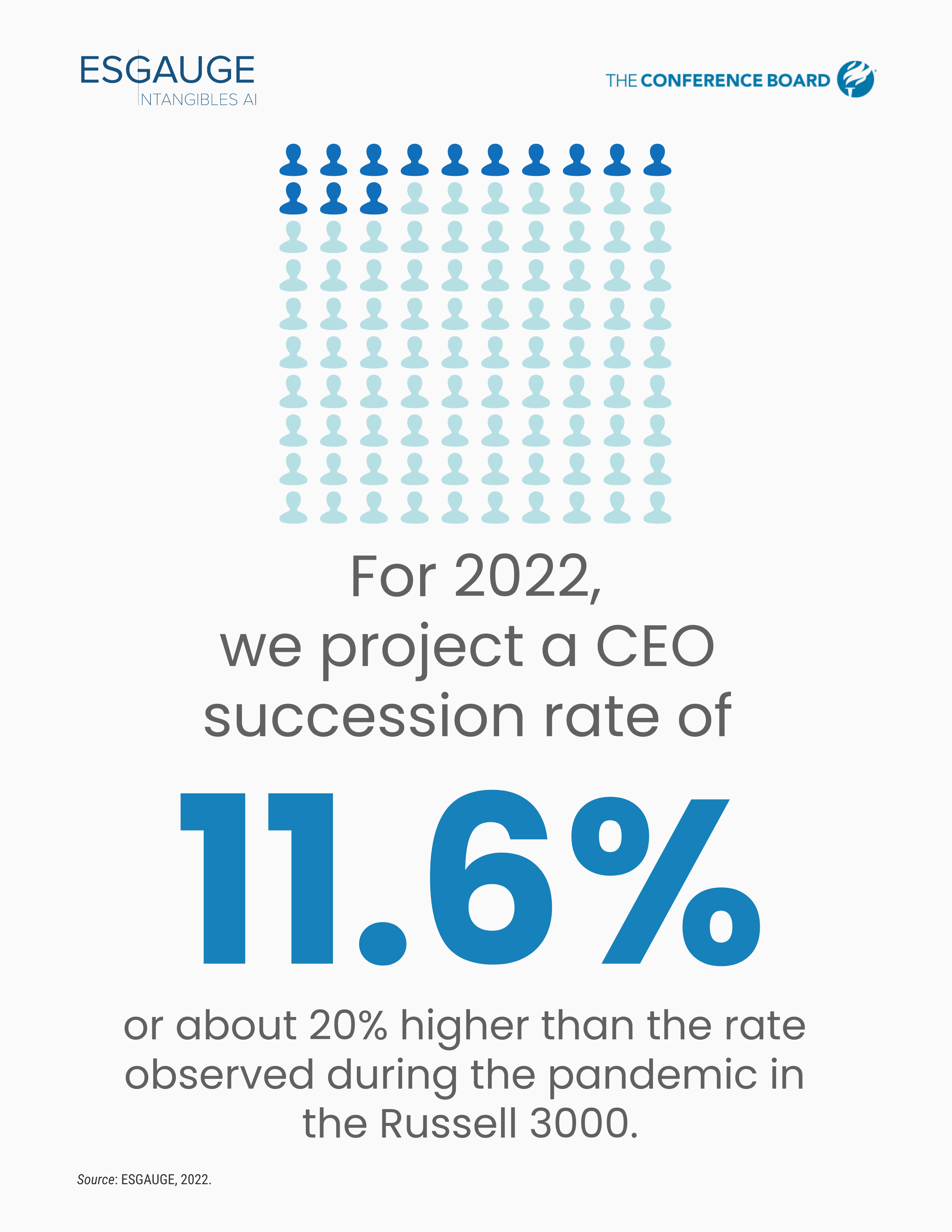

After declining during the pandemic, the rate of CEO turnover at US public companies is picking up rapidly, as boards regain confidence in their succession plans and recessions concerns prompts some longer-tenured leaders to exit their roles.

During the height of the pandemic, many companies chose to avoid compounding the business risks resulting from the crisis with the uncertainties of a leadership turnover. A clear decline in the 2021 rate of CEO succession indicated that, even in situations where a change might have been planned, many CEOs were asked to prolong their tenure and help to steer the ship. However, preliminary annualized data on the 2022 rate show that those earlier numbers may now be reversing and that this is poised to be a record year for CEO departures. Two factors may help to explain this finding.

During the height of the pandemic, many companies chose to avoid compounding the business risks resulting from the crisis with the uncertainties of a leadership turnover. A clear decline in the 2021 rate of CEO succession indicated that, even in situations where a change might have been planned, many CEOs were asked to prolong their tenure and help to steer the ship. However, preliminary annualized data on the 2022 rate show that those earlier numbers may now be reversing and that this is poised to be a record year for CEO departures. Two factors may help to explain this finding.

First, many CEOs are ready to move on. The pressure of managing during an unprecedented crisis—which, due to the current geopolitical and the looming prospect of a recession, has only accelerated rather than abated—has taken a toll on leaders, especially those who had been planned their retirement for years. Second, boards of directors may be more prepared for change too. In the last two years, they have had the time to stress-test and strengthen their company’s succession plan, gaining more confidence in their ability to execute it.