John Galloway is global head of investment stewardship at Vanguard, Inc. This post is based on a publication by Vanguard Investment Stewardship. Related research from the Program on Corporate Governance includes Social Responsibility Resolutions by Scott Hirst (discussed on the Forum here).

Risks to shareholder value associated with diversity, equity, and inclusion (DEI) remain a top engagement priority for Vanguard with our funds’ portfolio companies. Increased focus—from companies, regulators, investors, and employees—on racial and ethnic discrimination has heightened scrutiny of public companies’ DEI-related risks and opportunities, as have the COVID-19 pandemic and challenging economic conditions.

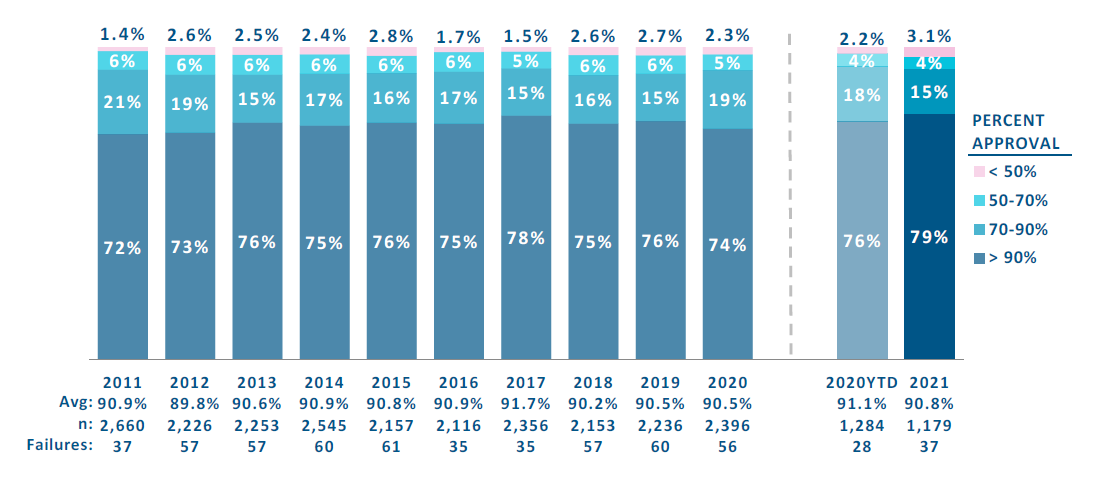

Vanguard has long advocated for diversity of experience, personal background, and expertise in the boardroom. In 2020, Vanguard continued to call for enhanced board diversity across dimensions of gender, race, ethnicity, age, and national origin. [1] We reiterated our expectations that boards make progress in their diversity strategy and that where progress falls behind market norms and expectations, the Vanguard funds may vote against company directors. We also outlined our views on diversity beyond the boardroom and our expectations of a board’s role in overseeing DEI risks within the workplace. [2] We illustrated the case for getting it right and the risks of getting it wrong.

Sidley Sends Formal Comment Letter on the SEC’s Universal Proxy Proposal

More from: Beth Berg, Derek Zaba, Holly Gregory, Kai Haakon Liekefett, Leonard Wood, Sidley Austin

Kai H.E. Liekefett, Derek Zaba, and Beth E. Berg are partners at Sidley Austin LLP. This post is based on a Sidley memorandum by Mr. Liekefett, Mr. Zaba, Ms. Berg, Holly J. Gregory, and Leonard Wood. Related research from the Program on Corporate Governance includes Universal Proxies by Scott Hirst (discussed on the Forum here); The Case for Shareholder Access to the Ballot by Lucian Bebchuk (discussed on the Forum here); and Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

On June 7, 2021, we sent a formal comment letter regarding the recent proposal of the U.S. Securities and Exchange Commission (SEC) to adopt a universal proxy (File No. S7-24-16) under the Securities Exchange Act of 1934 (as amended, the Exchange Act) (the Proposed Rule). We summarize our comments in this post (our full 20-page comment letter, including citations, can be reviewed here.

Since proxy contests are the context in which universal proxy cards would be used, we believe that our experience affords us with relevant perspectives on legal, procedural, and practical considerations. We have been involved in over 85 proxy contests in the past five years, more than any other law firm representing companies. In 2020, Sidley was ranked as the No. 1 legal advisor to companies in proxy contests by number of representations in the league tables maintained by Bloomberg, FactSet, Refinitiv (formerly Thomson Reuters), and Activist Insight.

READ MORE »