Dan Romito is Consulting Partner at Pickering Energy Partners. This post is based on his Pickering Energy Partners memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and For Whom Corporate Leaders Bargain (discussed on the Forum here) both by Lucian A. Bebchuk and Roberto Tallarita; Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock (discussed on the Forum here) by Leo E. Strine, Jr.; and Stakeholder Capitalism in the Time of COVID (discussed on the Forum here) by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita.

1. Blackrock’s voting “democratization” will gain popularity & eventual adoption by State Street & Vanguard, thereby adding yet another drain on management’s investor engagement resources

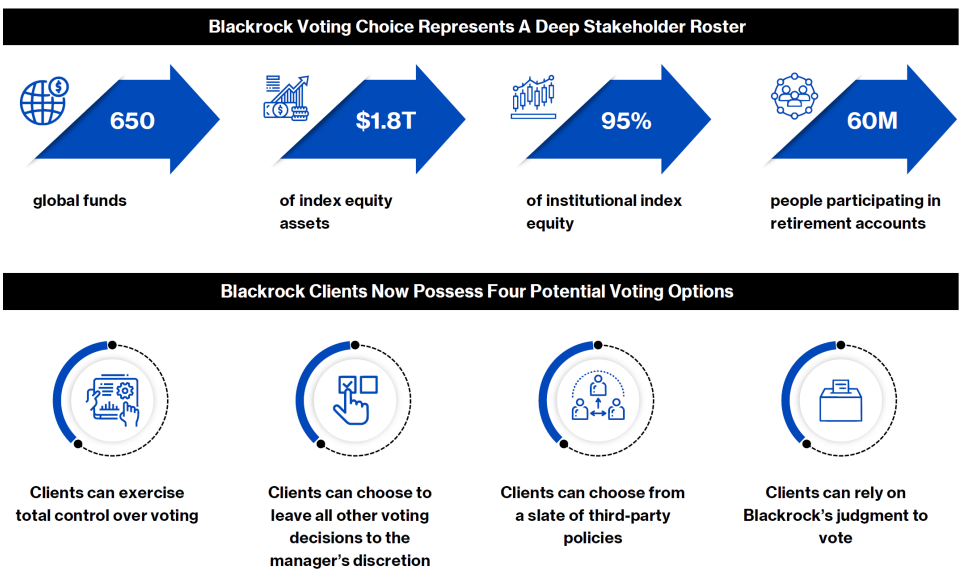

Larry Fink’s 2022 letter to CEOs outlines an unprecedented systematic change to proxy voting and marks a potentially disruptive inflection point within the conventional proxy voting process.[1] According to Blackrock, “this option gives institutional clients in separately managed accounts (SMAs) the ability to exercise their voting decisions on the topics or at the companies that matter most to them.” In other words, Blackrock has opened the door to an entirely new roster of complex stakeholders.

Blackrock’s client base now possesses the ability to directly vote on climate-related and human-capital-related issues. Mr. Finks’ letter specifically reinforces that “this new ecosystem will also pose challenges for CEOs and their companies. Those of us who lead public companies will have a broader set of shareholders with whom to engage. Companies may need to develop new models of engaging with asset owners on their most important voting matters. This may take time to evolve.”