Jeanne Hanna is Research Director, Bruce F. Freed is President and co-founder, and Karl J. Sandstrom is Strategic Advisor, at the Center for Political Accountability. Related research from the Program on Corporate Governance includes Corporate Political Speech: Who Decides? (discussed on the Forum here) by Lucian Bebchuk, Robert J. Jackson Jr.; The Untenable Case for Keeping Investors in the Dark (discussed on the Forum here) by Lucian Bebchuk, Robert J. Jackson, Jr., James Nelson, and Roberto Tallarita; The Politics of CEOs (discussed on the Forum here) by Alma Cohen, Moshe Hazan, Roberto Tallarita, and David Weiss; and Shining Light on Corporate Political Spending (discussed on the Forum here) by Lucian Bebchuk, and Robert J. Jackson Jr.

As the 2024 election cycle begins in earnest, companies must act on their fiduciary responsibility to more closely monitor their political spending and the accompanying risks. Too often corporate leaders fail to fully assess and scrutinize the ultimate beneficiaries of political contributions from corporate treasury funds. This oversight constitutes a lapse in corporate officers’ duty of care to protect and advance the interests of the company and its shareholders.

This duty is ever more crucial as corporate political engagement is increasingly scrutinized by the media, employees, investors, regulators, and consumers. This new reality has exponentially increased the financial risks companies face when their political spending directly or indirectly associates their brand with controversial political issues and outcomes and claims of corruption. Without the necessary due diligence, this new political landscape can also negatively affect the environment companies need to compete and operate in the long term and may expose a company to legal liability.

The Center for Political Accountability has spent the past two decades examining these risks as part of its effort to make corporate political disclosure and accountability a norm. Responsible business leaders must act on their legal obligations to protect companies from harm by increasing their scrutiny of corporate political spending and its ultimate beneficiaries and impacts. Companies can no longer give to politically active groups without giving close attention to the consequences or to what their political spending might enable. They must look behind the curtain and demand to know how their money is spent and what risks their company is assuming.

Risky Business

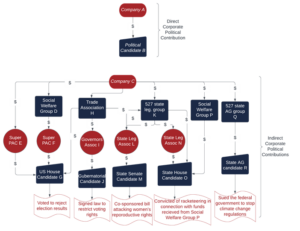

At both the state and federal level, public companies are often legally prohibited from donating to political campaigns or face strict limitations in how much they are allowed to donate directly to candidates.

Many companies, instead, choose to contribute indirectly to third-party groups –politically active trade associations; social welfare groups; partisan, state focused 527 committees; and super PACs — that engage in political spending and activities at both the state and national levels. These organizations then use the companies’ funds for election-related spending, often without informing corporate donors of their intentions. Corporate donations may be transferred to additional third-party groups before being spent on an election. Ultimately, a company’s donation may pass through several intermediaries before making its way to a final beneficiary (see Image below).

When companies donate to third-party groups, they typically lose the ability to control or to know how their money is eventually spent. Importantly, company leaders are frequently unaware of the issues and controversies the company may be associated with or what their money enables through the ultimate beneficiaries of their donations.

A 2021 report by the Center for Political Accountability illustrates how third-party contributions seriously undermined numerous companies’ commitments to democracy, addressing climate change, LGBTQ rights, reproductive healthcare, and other issues that are keenly tracked by consumers, employees, and shareholders. Careless political spending decisions can also place companies and corporate executives in legal jeopardy, as demonstrated by the recent investigations and federal criminal convictions associated with FirstEnergy in Ohio.

Indirect political donations and the ensuing controversies have repeatedly exposed a serious gap in corporate due diligence. This lapse has created serious risks that companies must confront.

Pull back the curtain & control the risk

To mitigate these risks, corporate leaders can and should demand a full accounting from all recipients of how its corporate treasury funds are spent. Companies should apply standards similar to those already in use to monitor and regulate corporate contributions to charitable and philanthropic organizations. Applying similarly robust standards of due diligence to their political giving enables corporations to pull back the curtain, assert the necessary control over their corporate funds and in doing so fulfill their fiduciary responsibilities.

The CPA-Wharton Zicklin Model Code of Conduct for Corporate Political Spending provides a framework for corporate leaders to apply due diligence, honor their duty of care, and manage risks associated with political spending. Specifically, the Code requires companies to obligate all trade associations and other third-party groups receiving corporate treasury funds that can be used for election-related spending to report to the company how its contributions are spent and who the ultimate beneficiaries of corporate funds are. This information empowers senior management and directors to more accurately assess the risks of that spending and to avoid the risks created by ill-considered spending.